All You Need to Know About the Foreign Earned Income Exemption and Its Link to the Common Reduction

The Foreign Earned Earnings Exclusion (FEIE) offers an important chance for U.S. people and resident aliens functioning abroad to decrease their taxed earnings. Comprehending the eligibility criteria and asserting procedure is vital. Nevertheless, the communication between the FEIE and the basic reduction can complicate tax technique. Bad moves in navigating these regulations can result in missed out on advantages. Checking out these aspects discloses important information for reliable tax obligation planning and taking full advantage of financial advantages.

Recognizing the Foreign Earned Earnings Exemption (FEIE)

The International Earned Earnings Exemption (FEIE) functions as an essential tax obligation provision for united state citizens and resident aliens who function abroad, allowing them to exclude a significant section of their foreign-earned earnings from united state federal tax. This provision is crucial for people living outside the USA, as it helps alleviate the economic worry of double taxation on earnings earned in international nations. By making use of the FEIE, qualified taxpayers can decrease their gross income significantly, advertising financial security while living and functioning overseas. The exemption amount is changed every year for inflation, ensuring it reflects existing financial conditions. The FEIE is particularly beneficial for those in regions with a higher expense of living, as it allows them to preserve more of their revenues. Understanding the mechanics and implications of the FEIE equips migrants to make informed economic choices and enhance their tax obligation situations while residing abroad.

Eligibility Needs for the FEIE

To certify for the Foreign Earned Revenue Exemption, people have to meet specific qualification demands that consist of the Residency Examination and the Physical Presence Test. Furthermore, employment standing plays a vital duty in determining eligibility for this tax obligation benefit. Recognizing these requirements is essential for any individual seeking to make use of the FEIE.

Residency Examination Standard

Determining qualification for the Foreign Earned Revenue Exclusion (FEIE) rests on meeting specific residency test criteria. Largely, individuals need to develop their tax obligation home in an international country and show residency via either the bona fide home test or the physical presence examination. The bona fide home test needs that a taxpayer has actually established a copyright in an international nation for an uninterrupted period that extends a whole tax year. This involves demonstrating intent to make the foreign area a principal home. Additionally, the taxpayer should exhibit ties to the foreign nation, such as protecting household, employment, or housing links. Meeting these residency requirements is crucial for qualifying for the FEIE and successfully decreasing tax responsibilities on gained income abroad.

Physical Visibility Examination

Meeting the residency requirements can additionally be achieved via the physical existence test, which provides an alternate path for qualifying for the Foreign Earned Revenue Exclusion (FEIE) To satisfy this examination, an individual need to be physically present in a foreign nation for at the very least 330 full days throughout a successive 12-month duration. This requirement emphasizes the significance of real physical presence, as opposed to just preserving a house abroad. The 330 days do not have to be successive, permitting adaptability in traveling setups. This test is specifically advantageous for U.S. locals or people functioning overseas, as it enables them to leave out a substantial portion of their foreign gained revenue from united state taxation, therefore lowering their general tax responsibility

Work Standing Requirements

Eligibility for the Foreign Earned Earnings Exclusion (FEIE) depends upon certain work status needs that individuals must meet. To qualify, taxpayers should demonstrate that their earnings is originated from international sources, generally via employment or self-employment. They need to be either a united state resident or a resident alien and maintain a tax obligation home in an international nation. Additionally, individuals have to meet either the Physical Visibility Examination or the Authentic Residence Examination to establish their international standing. Freelance individuals must report their web incomes, ensuring they do not go beyond the recognized exemption limitations. It's necessary for applicants to keep appropriate paperwork to corroborate their claims regarding work status and international income throughout the tax obligation year.

Just how to Declare the FEIE

Qualification Requirements Clarified

For people looking for to gain from the Foreign Earned Revenue Exclusion (FEIE), comprehending the qualification requirements is crucial. To qualify, one should satisfy two primary examinations: the authentic home test or the physical visibility examination. The bona fide home examination relates to those that have developed an irreversible home in a foreign nation for an uninterrupted period, normally a year or more. Conversely, the physical visibility examination needs people to be physically present in an international nation for at least 330 days during a 12-month duration. FEIE Standard Deduction. Additionally, only earned income from foreign resources gets exclusion. Satisfying these criteria is crucial for taxpayers desiring to lower their taxed earnings while residing abroad

Required Tax Return

Just how can one properly assert the Foreign Earned Earnings Exemption (FEIE)? To do so, details tax return must be made use of. The main kind required is internal revenue service Kind 2555, which allows taxpayers to report international earned earnings and claim the exemption. This type needs in-depth details regarding the person's foreign residency and the revenue made while living abroad. Furthermore, if declaring the exemption for housing prices, Form 2555-EZ may be made use of for simplicity, given certain requirements are satisfied. It is essential to assure that all needed sections of the kinds are completed properly to stay clear of hold-ups or problems with the internal revenue service. Understanding these forms is vital for taking full advantage of the benefits of the FEIE.

Filing Process Actions

Declaring the Foreign Earned Earnings Exclusion (FEIE) includes a collection of well organized and clear steps. Initially, individuals must identify their qualification, confirming they fulfill the physical visibility or bona fide home examinations. Next, they must finish internal revenue service Type 2555, describing revenue gained abroad and any relevant exclusions. It is important to gather supporting documents, such as international income tax return and proof of house (FEIE Standard Deduction). After filling out the form, taxpayers should affix it to their yearly tax return, commonly Form 1040. Declaring digitally can improve this process, yet ensuring precise information is vital. Lastly, people must keep duplicates of all submitted types and sustaining files for future reference in situation of audits or queries from the IRS

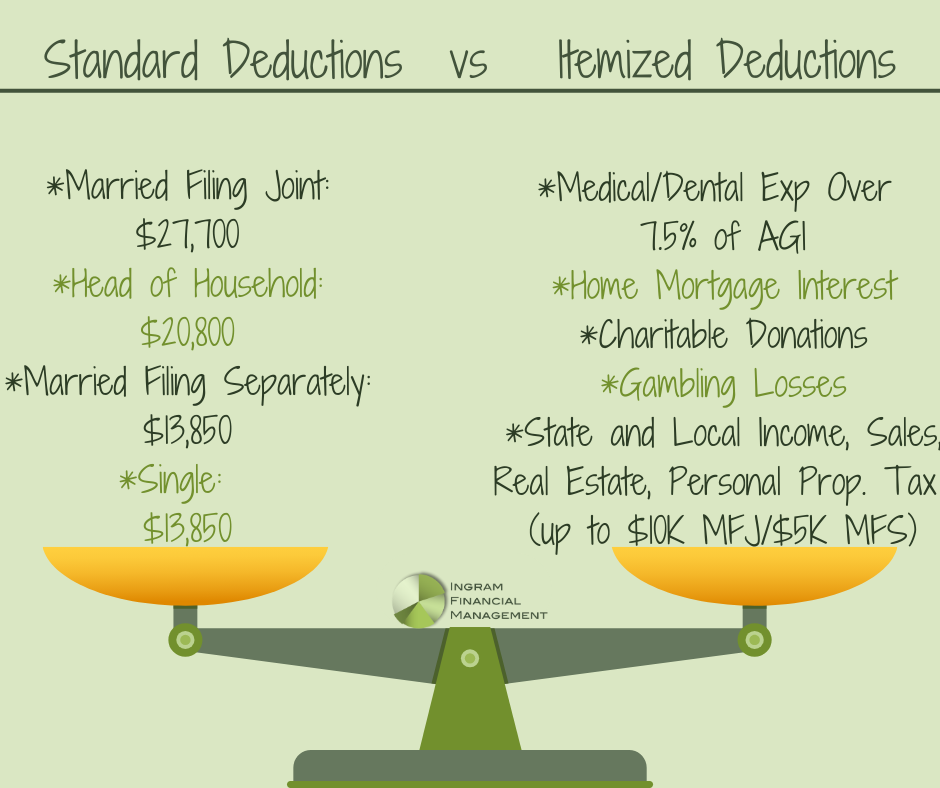

The Requirement Deduction: A Review

The common deduction serves as a crucial tax obligation benefit that simplifies the filing process for lots of people and households. This deduction permits visit this page taxpayers to decrease their gross income without the need to make a list of reductions, making it an appealing alternative for those with uncomplicated economic scenarios. For the tax obligation year, the conventional reduction amount varies based on declaring condition, with various limits for single filers, couples filing jointly, and heads of house.

The common reduction is changed annually for rising cost of living, guaranteeing its relevance gradually. Taxpayers that qualify can pick between the typical deduction and itemizing their reductions, commonly opting for the greater advantage. By providing a baseline deduction, the common deduction sustains taxpayers in decreasing their overall tax liability, therefore boosting their financial setting. Understanding the basic reduction is vital for reliable tax preparation and taking full advantage of prospective savings for individuals and family members alike.

Interaction Between FEIE and Common Deduction

While both the Foreign Earned Revenue Exclusion (FEIE) and the basic reduction serve to minimize taxable income, their communication can substantially impact a taxpayer's total tax obligation liability. Taxpayers who qualify for the FEIE can exclude a significant quantity of their foreign-earned earnings, which may influence their eligibility for the standard deduction. Particularly, if a taxpayer's foreign income is entirely excluded under the FEIE, their gross income may fall below the threshold essential to assert the conventional deduction.

It is important to note that taxpayers can not double-dip; they can not make use of the very same income to assert both the FEIE and the common reduction. This suggests that cautious consideration is required when identifying the ideal method for tax obligation reduction. Eventually, understanding exactly how these two stipulations communicate enables taxpayers to make enlightened decisions, guaranteeing they optimize their tax obligation advantages while remaining compliant with internal revenue service laws.

Tax Benefits of Making Use Of the FEIE

Making Use Of the Foreign Earned Income Exclusion (FEIE) can give remarkable tax obligation advantages for united state citizens and resident aliens living and functioning abroad. This exclusion enables qualified people to omit a specific amount of foreign-earned income from their gross income, which can lead to substantial tax savings. For the tax year 2023, the exemption quantity is up to $120,000, noticeably lowering the gross income reported to the IRS.

Furthermore, the FEIE can aid avoid double taxation, as international taxes paid on this revenue may also be eligible for credit histories or reductions. By strategically using the FEIE, taxpayers can preserve even more of their income, permitting for enhanced monetary stability. Furthermore, the FEIE can be helpful for those who get the bona fide residence examination or physical visibility examination, offering adaptability in managing their tax commitments while living overseas. Generally, the FEIE is an important tool for expatriates to optimize their funds.

Usual Errors to Avoid With FEIE and Basic Deduction

What challenges should taxpayers recognize when claiming the Foreign Earned Revenue Exclusion (FEIE) alongside the conventional deduction? One common error is presuming that both advantages can be asserted all at once. Taxpayers should recognize that the FEIE should be asserted prior to read this the standard reduction, as the exemption fundamentally minimizes gross income. Falling short to meet the residency or physical visibility tests can likewise result in ineligibility for the FEIE, causing unanticipated tax obligation responsibilities.

Additionally, some taxpayers neglect the need of proper documents, such as keeping documents of international revenue and traveling days. One more constant error is overlooking the exclusion amount, possibly due to wrong forms or false impression of tax regulations. Ultimately, people should bear in mind that claiming the FEIE might affect qualification for particular tax credit scores, which can complicate their total tax obligation scenario. Recognition of these pitfalls can help taxpayers navigate the complexities of global taxes better.

Regularly Asked Questions

Can I Declare FEIE if I Live Abroad Part-Time?

Yes, an individual can declare the Foreign Earned Revenue Exclusion if they live abroad part-time, given they fulfill the necessary demands, such as the physical visibility or authentic residence examinations outlined by the IRS.

Does FEIE Influence My State Tax Obligation Responsibilities?

The Foreign Earned Revenue Exemption (FEIE) does not directly affect state tax obligation commitments. States have varying regulations pertaining to revenue earned abroad, so people should consult their details state tax regulations for exact guidance.

Are There Any Type Of Expiry Dates for FEIE Claims?

Foreign Earned Income Exemption (FEIE) claims do not have expiration days; nonetheless, they should be claimed yearly on income tax return. Failure to claim in a given year may lead to lost exclusion benefits for that year.

Exactly How Does FEIE Impact My Social Safety Advantages?

The Foreign Earned Earnings Exclusion (FEIE) does not straight impact Social Security advantages, as these benefits are based upon lifetime revenues. Nevertheless, omitted revenue might reduce overall profits, possibly affecting future benefit computations.

Can I Withdraw My FEIE Claim After Submitting?

Yes, an individual can revoke their Foreign Earned Income Exclusion claim after filing. This abrogation needs to be submitted via see here the suitable tax types, and it will certainly affect their tax obligation commitments and possible reductions progressing.

The Foreign Earned Earnings Exclusion (FEIE) offers an important chance for United state residents and resident aliens working abroad to reduce their taxable earnings. Comprehending the Foreign Earned Income Exemption (FEIE)

The Foreign Earned International Exclusion (Exemption) serves as offers essential tax provision tax obligation Arrangement citizens and resident aliens who work abroadFunction allowing them to exclude a leave out portion of part foreign-earned income from U.S. federal taxationGovernment While both the Foreign Earned Earnings Exemption (FEIE) and the typical reduction offer to decrease taxable earnings, their communication can significantly impact a taxpayer's overall tax liability. Making Use Of the Foreign Earned Income Exemption (FEIE) can offer significant tax obligation benefits for United state people and resident aliens living and functioning abroad. Foreign Earned Earnings Exclusion (FEIE) claims do not have expiry dates; however, they should be asserted annually on tax returns.